For foreign nationals employed in Vietnam, a comprehensive understanding of the tax landscape is the prerequisite for financial compliance and strategic planning. The regulations regarding Vietnam PIT rates diverge significantly based on the individual’s legal residency status.

This guide elucidates the statutory classification of tax resident vs non-resident Vietnam, the applicable taxation regimes, and the essential protocols regarding tax finalization for foreigners.

1. Statutory Determination of Tax Residency

The primary determinant of tax liability is the individual’s residency status. Pursuant to Article 2 of the Law on Personal Income Tax, a foreign national is legally classified as a Tax Resident if they satisfy either of the following statutory conditions:

- Physical Presence: The individual is present in Vietnam for 183 days or more within a calendar year or within 12 consecutive months commencing from the first date of arrival.

- Permanent Residence: The individual maintains a regular place of residence in Vietnam, which includes either a registered permanent residence or a rented domicile under a fixed-term contract.

Non-Resident Status: Foreign nationals who fail to meet the aforementioned criteria are classified as Non-Residents. This legal distinction dictates the applicable tax tariff and the scope of taxable income.

2. Applicable Tax Regimes: Resident vs. Non-Resident

A. For Tax Residents

Tax Residents are subject to taxation on their worldwide income, encompassing income generated both within and outside the territory of Vietnam.

For income derived from salaries and wages, Residents are subject to the Partially Progressive Tax Tariff. Under Article 22, tax liability increases incrementally with income, capped at a maximum marginal rate of 35%.

Statutory Tax Brackets:

- Level 1: Up to 60 million VND/year (5 million/month) — 5%

- Level 2: Over 60 to 120 million VND/year — 10%

- Level 3: Over 120 to 216 million VND/year — 15%

- Level 4: Over 216 to 384 million VND/year — 20%

- Level 5: Over 384 to 624 million VND/year — 25%

- Level 6: Over 624 to 960 million VND/year — 30%

- Level 7: Over 960 million VND/year (over 80 million/month) — 35%

Legal Note: Tax Residents are entitled to family circumstance deductions (for the taxpayer and qualified dependents) prior to the calculation of taxable income.

B. For Non-Residents

Non-residents are liable for tax solely on income sourced within Vietnam, irrespective of where the income is paid or received.

The taxation mechanism is a flat rate system that does not permit personal deductions. Pursuant to Article 26, the tax liability on salaries and wages is calculated by applying a flat rate of 20% to the total taxable income.

3. Tax Finalization & Refunds

Tax finalization for foreigners refers to the mandatory procedure of reconciling tax liabilities with the state budget at the conclusion of the fiscal year or prior to permanent departure from Vietnam.

Statutory Obligations

- Withholding Agent Responsibility: Income-paying organizations (employers) are legally mandated to withhold and finalize tax on behalf of authorized employees.

- Individual Responsibility: Individuals must directly file for tax finalization if they have outstanding tax obligations (underpayment) or if they elect to claim a tax refund.

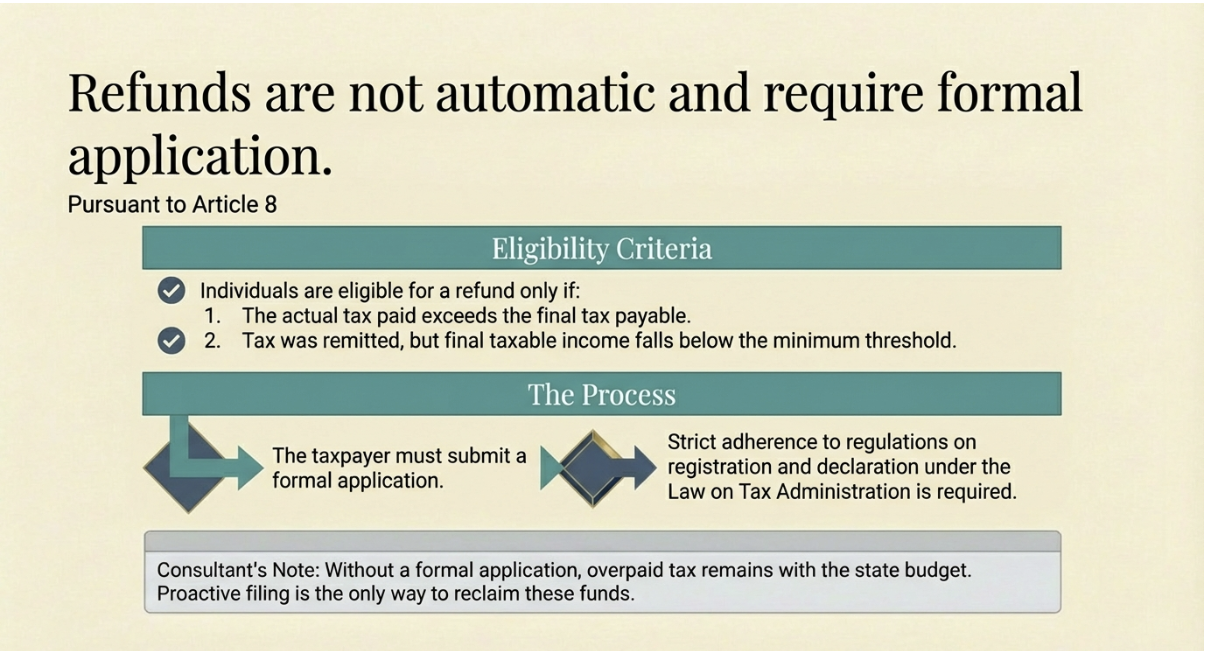

Tax Refunds

Overpayment of taxes does not trigger an automatic refund; the taxpayer must submit a formal application. Under Article 8, an individual is eligible for a refund in the following instances:

- The actual tax paid exceeds the final tax payable.

- The individual has remitted tax, but their final taxable income falls below the minimum threshold for taxation.

Procedural Compliance: To effectively claim a refund or finalize tax obligations, foreign nationals must strictly adhere to the regulations governing tax registration, declaration, and deduction as stipulated in the Law on Tax Administration.

📞 Contact DHH Law Firm Today

Confused by the Progressive Tax Tariff or the specific deductions available to you? Calculating exact liability and handling tax finalization for foreigners upon repatriation requires precision.

🏢 Main Office: 2nd Floor, 829 Huynh Tan Phat Street, Phu Thuan Ward, Ho Chi Minh City, Vietnam

📞 Hotline:

- +84 89 9352 777 (Vietnamese)

- +84 89 9351 777 (English)

🌐 Website: www.dhhlawfirm.vn

📧 Email: contact@dhhlawfirm.vn

✨ DHH Law Firm – Your trusted legal partner for family and foreign-related civil procedures in Vietnam.